David McCarthy

David McCarthy teaches Risk Management and Insurance at the Terry College of Business of the University of Georgia. His research focuses on pension and retirement-related issues at the international, national, and individual levels.

Ask yourself these questions:

- Do you want a guaranteed retirement income stream as long as you live, to protect you against outliving your assets?

- Are you nearing retirement?

- Are you in a defined contribution pension – either an employer-sponsored 401(k) or 403(b) plan, or an individual Roth or regular IRA?

If the answer to any of these questions is “yes,” reading this post could save you money!

Shop Around for the Right Income Solution for You

When you retire and start using your savings to provide an annual income, it is best to do so as cost-effectively as possible. Buying a higher-cost retirement income product than you need to will mean you’ll need to work longer, save more, or spend less when you’re retired. Frankly, why do any of these things if you don’t have to?

In the US, many types of retirement income products are available. The simplest is called an immediate annuity, which is an insurance product that converts a lump sum of money into a guaranteed lifetime income. Despite their simplicity and relative transparency, these products are not popular in the US. Jonathan Lindvig, a financial planner at Peachtree Wealth Advisors in Atlanta, GA, says: “With interest rates at record lows and increases in longevity, payout rates of immediate annuities have fallen, and many people are choosing to purchase variable annuities rather than immediate annuities when they retire.”

Variable Annuities

Variable annuities are tax-preferred hybrid products that provide purchasers with the option – at a cost – to buy a guaranteed lifetime income, while also letting them choose which underlying assets to invest in. If these assets perform well, income may be greater than the guaranteed level (and the guarantee itself may increase). Many variable annuities offer guaranteed income rates that are not much lower than the payout rates on immediate annuities, so purchasers choosing the guaranteed income option get a guaranteed income that, although perhaps at first a little lower than the income provided by an immediate annuity, could rise in the future.

Another reason that many purchasers favour variable annuities is that if they die early, the balance in the annuity is paid over to their estate, rather than reverting to an insurance company as it does in the case of an immediate annuity. Unlike immediate annuities, variable annuities can also be surrendered, making the purchase less stressful (although some providers may add charges if you terminate the policy early).

Despite these advantages of variable annuities, those approaching retirement should still consider immediate annuities. Some reasons why are discussed below.

Charges on variable annuities are often much higher than those on simple mutual funds, sometimes higher than 3% p.a., and the impact of these fees accumulates the longer you hold the annuity. These high charges mean that the average returns on asset portfolios from the date you bought the policy must be as high as 8% or 9% p.a. before fees before income – guaranteed or otherwise – can increase. If asset returns are low, especially in the first few years after buying the variable annuity, immediate annuities may provide a higher income in the long run.

Immediate Annuities

The older you are, the more likely it becomes that immediate annuities are a better choice. This is because the guaranteed income rates offered under variable annuities do not generally increase as much with age as the pay-out rates of immediate annuities. Buying a cheap mutual fund for the first few years after retirement, especially if your funds are already in tax-preferred vehicles such as a 401(k) or an IRA, and only then buying an immediate annuity, will save you the high variable annuity expenses and may often prove to be a better choice than choosing a variable annuity with a guaranteed income option immediately.

Variable annuities can also be very complex, with many possible underlying choices and policy conditions. This can make them difficult to compare across providers before you buy, and stressful and complicated to operate afterwards.

Immediate annuities are much easier to compare than variable annuities – once you have chosen some basic product features, all that matters is the level of income and the financial strength of the insurance company. They also operate automatically after they have been purchased, making for a stress-free and predictable retirement. But selecting the right immediate annuity to buy is important because you generally cannot switch to a different provider if you change your mind or uncover a better deal later. The immediate annuity you pick at retirement, good or bad, is yours for life.

If all insurers charged the same for immediate annuities, it wouldn’t be worthwhile to shop around. But annuity rates do differ across providers, especially if you have an underlying health condition, or if you smoke. For this reason, shopping around may boost your retirement pay-outs a lot.

Some Examples

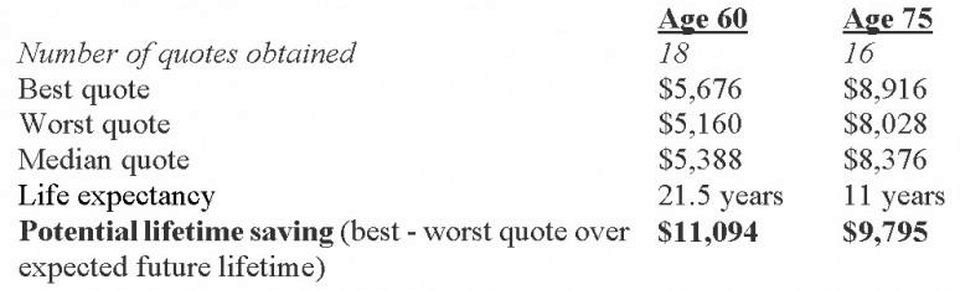

We illustrate what astute immediate annuity selection can mean by comparing recent quotes from a range of large US insurance providers. The quotes were obtained for males age 60 and 75, resident in Georgia, and in good health. The table shows the annual income from the annuity per $100,000 of principal.

Quotes differ by as much as 10% for the 60 year-old, and 11% for the 75 year-old. These translate into potential savings of more than 11% of the initial principal over the expected future lifetime of the younger individual, and nearly 10% of the principal for the older one.

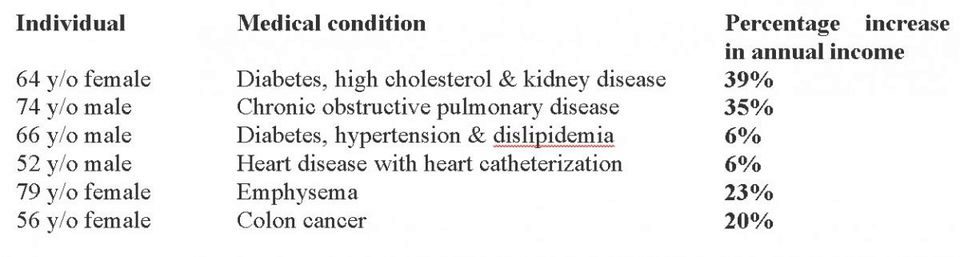

And note, if you have an underlying health condition, your savings could be much greater. Some providers will pay you more than they would if you were fully healthy, reflecting your lower life expectancy – the opposite of regular life insurance. Some recent real-world examples from the US are shown in the table below, derived using www.immediateannuities.com.

These examples illustrate how important it is to shop around when considering purchasing an immediate (or variable) annuity. A little time spent reviewing annuity quotes before retirement could be time very well spent! Even 10% more income during retirement means that you can save less while you are working, retire earlier, or spend more money after you are retired.

What Are Regulators Doing About This?

Regulators around the world have become concerned about the potential for people to lose a great deal of retirement income when they don’t shop around. In the UK, for instance, they’re working on a requirement that pension providers show people – in real money terms – how much they can gain by accepting alternative quotes for immediate annuities. The UK’s Financial Conduct Authority (FCA) is building a new online tool to show savers the best available rates on different annuity products and compare them to their employers’ offers. In Chile, an online auction system shows retirees all the available annuities and ranks them in order of price.

In the US context, J. Mark Iwry of the US Treasury Department has stated that the Federal government wants to help Americans buy annuities to make their retirement savings last. Additionally many providers such as Vanguard offer investors assistance in shopping around for immediate annuities, and there are also online brokers specialising in annuities.

Christopher Woolard of the FCA has stated: “Deciding how to use pension savings is one of the most important decisions people will make. For a competitive and innovative market, it’s crucial that the market develops in a way that allows consumers to engage with their options, shop around, and switch providers where appropriate. We also want firms to compete hard for business, offering good outcomes for consumers through lower prices, products and services that meet customer needs, better customer service and wider choice.”

What Can You Do?

To do the best you can in retirement, you’ll need to get the best quality information possible. Here are some simple things you can do to help you get a better deal:

- Educate yourself. The internet can be a great place to start, but don’t buy before you compare. To use financial advisors effectively, it helps to know a little about what your options are.

- Shop around. Retirement is an emotional time, but brand loyalty is often misplaced and is sometimes abused. People often forget that annuities are different from regular insurance. With annuities, you may get a better deal if you can prove that you are sick, not if you show that you are healthy.

- Be sceptical. If a deal or product seems too good to be true, it often is!

- Find a good financial advisor or financial planner. It’s better if you can pay them directly, like you pay your dentist, rather than if they rely on commissions from product providers. If you can’t find an advisor who will accept a fee-for-service charging model, make sure you know which products the advisor is contractually permitted show you and how much commission he or she earns on each of the options. If you do use on-line brokers, be sure you understand how they have selected the companies they provide quotes for, and how they are remunerated for their services.

This piece was originally posted on August 28, 2016, on the Pension Research Council’s curated Forbes blog. To view the original posting, click here.

Views of our Guest Bloggers are theirs alone, and not of the Pension Research Council, the Wharton School, or the University of Pennsylvania.