James Moore is President of Avalana Advisors. Previously he was a Managing Director at PIMCO. He has a PhD from the Wharton School of the University of Pennsylvania.

Between 1960 and 2018, poverty among the US elderly fell from 35% to 9.7%. This was a direct result of changes made to Social Security and the introduction of Medicare in 1964. Social Security provides forced retirement savings for nearly all workers in the US, along with a wealth transfer from high earners to the poor and disabled given its progressive benefit structure. In 2019, 64 million Americans received Social Security benefits – more people than those who voted for our President.

But is Social Security sustainable on its current path? Valued under the assumptions used by the Social Security Administration’s (SSA) Actuaries, there is reason for concern. Valued using market interest rates, the unfunded future obligations are daunting.

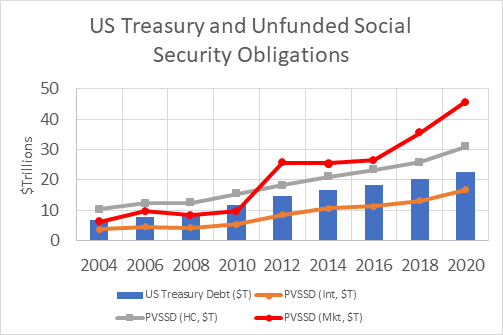

Figure 1 below compares the present value of social security deficits (PVSSD) under three assumptions regarding the value of outstanding market-traded US Treasury debt, for valuation dates over the past 16 years. The blue bars show outstanding market-traded Treasury debt, and the lines present the PVSSD for three assumptions: Intermediate (orange), High Cost (gray) as provided by the Social Security Administration’s (SSA) annual report, and my estimates (red) using market interest yields on Treasury Inflation-Protected Securities (TIPs) at the corresponding valuation dates. Between 2004 and 2020, under the intermediate assumptions, PVSSD has grown from $3.7T to $16.8T, or from 54% to 74% of outstanding public market debt. Under the high cost assumptions, the corresponding numbers triple in value from $10.3T to $30.9T. Using market yields, the PVSSD has rocketed from $6.2T to $45.6T, or from 91% to twice the value of market-traded Treasury securities.

| Figure 1 – Outstanding Treasury and Unfunded Social Security Obligations |

|

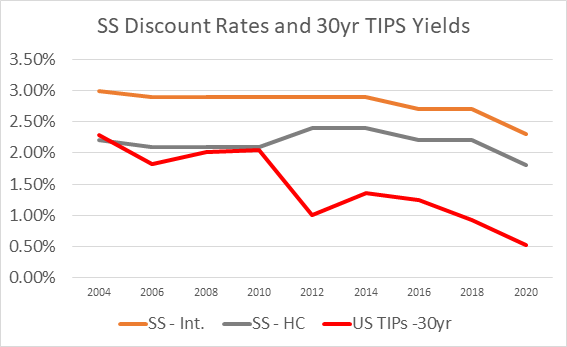

What assumptions change across these estimates? None other than substituting the market yield on 30-year TIPs for the interest rates used in the SSA’s Intermediate Scenario. Figure 2 shows the TIPs yield versus the assumed real interest rate used in the SSA Actuarial Report for the years 2004-2020. In 2004, the high cost interest rate assumption was lower than the TIPs yield, and through 2010 these two remained relatively close. After 2010, however, market yields diverged substantially from the SSA discount rate assumptions, and very worrisomely, they are moving further apart. Since 2014, SSA assumed interest rates have trended downward, but less quickly than market rates moved. Between 2004 and 2020, the spread between the Intermediate ultimate real rate assumption and the TIPs yield widened from 0.7% to 1.8%. Also bear in mind that the last rate shown was for September 30, 2019, before the Covid-19 pandemic. As of September 30, 2020, the market TIPs yield was -0.33%, which would imply the 2021 unfunded estimates will be far worse.

| Figure 2 – Social Security Real Discount Rate Assumptions and 30-yr TIPs Yields |

|

The 2020 SSA Actuarial Report runs to 276 pages. It presents a bewildering array of tables and numbers, but nowhere does it present a valuation estimate of the system using easily obtained current market rate assumptions. To generate this requires a thorough reading of the report and its appendices to recognize key inputs and gain understanding of the valuation process, as well as a bit of high school algebra.

Major modifications to Social Security were last made in 1983 when normal retirement ages were slowly raised. Both Presidents Bush (2001) and Obama (2010) empaneled bi-partisan commissions to study the system’s continuing problems, and both times nothing was done. Valued using market rates, Social Security’s unfunded is now 4.7 times what it was in 2010. A problem deferred is a problem compounded.

Implications:

- Social Security’s finances are in much worse shape than decisionmakers and the American public realize. By using optimistic, off-market assumptions and burying the most important numbers, the Actuaries and Trustees have contributed to complacency. Congress and the executive branch need good numbers to make decisions, but they have yet to receive them.

- Washington has kicked the can down the road for too long. It has been 37 years since anything truly substantive was done to address Social Security’s fiscal deficits. Those insufficiencies, once small cracks, have eroded into a yawning chasm.

- Tough decisions must be made soon. Many Americans want to see benefits increased, and they’d also like to see a second round of stimulus during these difficult times. Who can tell them the news they don’t want to hear? Our nation faces tough choices between cutting benefits and raising taxes now on lifetime promises. If not, our children and grandchildren will be burdened with a bill beyond comprehension.

This is a shortened version of a longer article, which you can read here.

Views of our Guest Bloggers are theirs alone, and not of the Pension Research Council, the Wharton School, or the University of Pennsylvania.