Abigail Hurwitz and Orly Sade

Abigail Hurwitz is a lecturer at the College of Management Academic Studies, Israel and a visiting scholar at The Wharton School of the University of Pennsylvania. Orly Sade is an Associate Professor of Finance at the Department of Finance, School of Business Administration, Hebrew University of Jerusalem, and a Visiting Associate Professor at the Stern School of Business, NYU.

Smoking and Self-Assessed Longevity

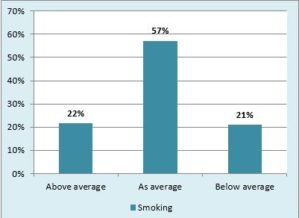

We have recently explored this question focusing on smokers, since smoking is widely confirmed to reduce human life spans. Our research reveals a stunning gap between objective life expectancy and how smokers think about their own life spans. To examine this point, we asked 963 in a representative sample in Israel whether they thought they would live as long as, less than, or longer than an average person. Strikingly, 57% anticipated having an average span, 22% believed they would live longer than average, and only 21% said they expected a shorter lifetime than the norm (Figure 1). In other words, 79% of smokers believed that they would live just as long, or even longer than, the general population.

Smoking and Self-Reported Health

We further asked the respondents to self-assess their own health by rating themselves on a scale of 1 (very good health) to 4 (poor health). Smokers, former smokers, and nonsmokers all provided similar self-assessments: in fact, smoking was not significantly related to health perceptions or self-assessed life expectancies! And controlling for other factors, the average smoker in our survey did not perceive her- or himself as any less healthy than a nonsmoker, even though medical studies show smokers take 10 years off their lives on average.

Our results are consistent with US evidence: overall, heavy smokers are overoptimistic about their longevity. Moreover, they tend to more open to information denying a smoking–cancer link, versus nonsupportive information. These results also agree with studies regarding smokers’ health perceptions. For instance, only 29% of US smokers report that their own risk of heart attack is higher than average, and only 40% believe they are at greater than average risk of cancer.

Does Longevity Optimism Carry Over to Retirement Decisions?

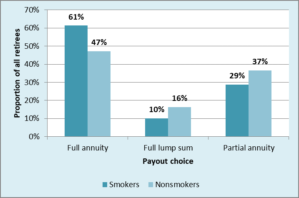

We then asked whether such longevity optimism carried over to financial decisions people make regarding their retirement. This is feasible to do in Israel since pricing of longevity annuities does not take into account buyers’ health or smoking status. This means that (other factors equal), smokers and non-smokers are offered an identical payout for a given premium. Moreover, if smokers know they will have shorter lives on average, they would be expected to prefer lump sums over lifetime benefit payments.

Again, we were surprised to learn smokers do not favor the lump-sum payout option compared to nonsmokers. In fact, the Figure below shows that 61% of smokers elected full annuities, while only 47% of nonsmokers chose that option.

Lessons Learned

Lessons Learned

Financial advisors and prospective retirees can learn from our work, which reveals that people – in this case, smokers – have over-optimistic perceptions about their remaining lifetimes. Such misconceptions can influence their financial decisions, and in turn, whether they leave their surviving family members with adequate retirement security.

Views of our Guest Bloggers are theirs alone, and not of the Pension Research Council, the Wharton School, or the University of Pennsylvania.